Project Info:

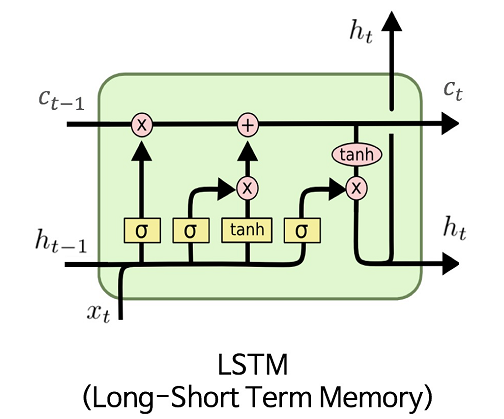

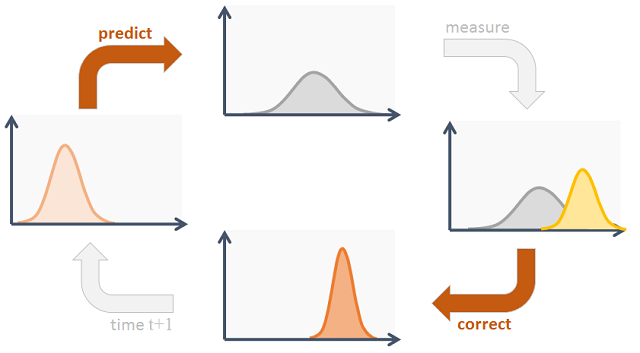

This project is a continuation and advancement of the HFT project, part of the FIN 556 course project. We implemented two strategies: LSTM and Kalman filter. The LSTM model is trained by Pytorch in Python first, then integrated in the C++ Srategy Studio environment to make inference/predictions, which are used for backtesting. The Kalman filter is directly coded in C++ by implemented the Strategy Studio interface.

Project Details:

- Authors:Ruipeng Han, Tomoyoshi Kimura, Sherlock Jian, Kaiyuan Luo

- Category:Finance, Machine Learning

- Technologies:Pytorch, C++, Linux, Strategy Studio (backtesting software)

- Date:Dec, 2022

- Github:https://github.com/tomoyoshki/HFT-strategies

Share: